Public Announcements

Notice Regarding Membership Dues for Fiscal Year 2025–2026

OPM Response To GFOA-CT Letter

Please see below for a letter from the State of Connecticut Office of Policy & Management in response to the GFOA-CT's February 24, 2025 letter to State Legislators and Elected Officials regarding the challenges faced by Connecticut municipalities during the fiscal year 2026 budget development process as a result of recent legislation.

Government Finance Officers Association of Connecticut

Kevin Redmond, GFOA CT President

400 Main Street

Ridgefield CT 06877

Via email: [email protected]

Dear Mr. Redmond:

Thank you for your letter on behalf of the Government Finance Officers Association of Connecticut (GFOA) regarding concerns in the municipal budget development process.

Governor Lamont recently signed House Bill 7067 on March 3, 2025. The bill implements several provisions including (1) creating an option for municipalities to adopt a modified depreciation schedule for motor vehicles, and (2) adjusting the property tax exemption for permanently and totally disabled veterans.

Additionally, the House and Senate passed this week House Bill 7163, An Act Concerning Emergency Grants to Municipalities for Special Education that invests an additional $40 million in special education services for municipalities this year.

Over the Governor’s term, we have significantly increased municipal aid over these eight budgets, including investments that have more than doubled funding for PILOT grants. The Governor’s budget fully funds all general government statutory formula and payment list grants from the Municipal Revenue Sharing Fund. This includes an increase from $60 million to $91 million in the Municipal Grants in Aid over the years, which was established to aid municipalities when the manufacturing machinery and equipment grant program ended.

Of note, municipalities have an accumulated $25 million Local Capital Improvement Program funds that they have not requested from fiscal year 2023 and prior, and they reported not utilizing $31 million of their fiscal year 2024 funds. These funds aid municipalities in their budgets and would assist in lowering their mill rates if fully utilized.

The Governor’s budget additionally proposes incentivizing municipalities to share services, which will enhance regional cooperation and lead to reduced costs, improving services to and affordability for local taxpayers. To do so, Governor’s Bill 6865 directs $250,000 in funds from the regional planning incentive account (RPIA) to each regional council of government to support positions for (1) stormwater management and flood mitigation and (2) regional municipal solid waste and recycling. The coordinators will help build capacity by providing services and programs on a regional scale in support of the state’s policy objectives. Regional approaches will enhance services and mitigate the burden on local property taxpayers.

Undersecretary

GFOA-CT Letter to State Legislators and Elected Officials

February 24, 2025

State Legislators and Elected Officials,

As you are aware, for decades the car tax in Connecticut has been based on fair market value and recently with a mill rate cap of 32.46. With the passage of Public Act 22-118 and 2024 Special Session Public Act 24-1, municipalities throughout the state now assess motor vehicles based on Manufacturer Suggested Retail Price (MSRP). A standardized depreciation schedule is applied to the MSRP, based on the age of the vehicle, and the depreciated value is multiplied by the statewide assessment ratio of 70% to arrive at a taxable assessment.

As a result of this change, effective for the October 2024 Grand List, cities and towns in Connecticut are facing severe losses in motor vehicle assessments. The consensus across all 169 Connecticut municipalities is an average decrease of 12%-16%. In Manchester, for example, the change resulted in an assessment loss of $81 million, or a 16.4% decrease from the previous year. Likewise, Glastonbury experienced a net assessment loss of $41.2 million, or 9.6%, while West Hartford dropped $50 million, or 8.5%.

Public Act 24-46, which expands property tax exemptions for Veterans, further decreased municipal grand lists by millions of dollars. The sheer number of Veterans eligible under Public Act 24-46 grossly exceeds the estimated statewide impact indicated by the $4.9 million fiscal note attached to the bill. For example, Manchester saw a $5 million decrease in its grand list alone; Colchester dropped $275,000; Stratford lost $2.8 million, and Norwich will see a decrease of $140,000 due to the new exemption.

Given the statewide impact of the new motor vehicle assessment formula, GFOA-CT is humbly suggesting the following potential legislative solutions to ensure that the fiscal impact that comes with the burden of funding government might be offset to Connecticut’s property taxpayers:

-

-

- Real Estate and Personal Property would remain at 70%; but this change would significantly offset the negative impact of PA 22-118.

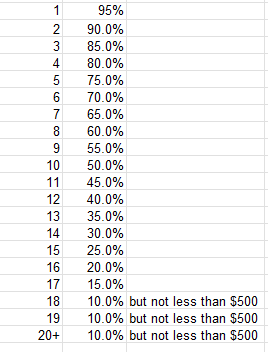

- A more elongated schedule would have less impact on assessment values. For example, the following schedule would gain 10% more value for every year up to 14 years:

- Resume reimbursing municipalities for the state-mandated 100% property tax exemption for machinery and equipment (MME).

- Since the 2011 assessment year, state law has exempted all MME from local property tax. Prior to 2011, new and newly acquired MME was exempt for the first five years after it was acquired and, from 2006 to 2010 assessment years, MME that was six years old or older was exempt under a five-year phase-in schedule (PA 06-83). The state does not currently reimburse municipalities for the MME exemption, although it does provide bond-funded municipal aid grants that are indirectly designed to mitigate a portion of the revenue loss from the exemption. Prior to FY 12, the state reimbursed municipalities for part or all of the revenue loss attributed to the MME exemption (along with a separate exemption for certain commercial vehicles) through a payment in lieu of taxes (PILOT) grant. Beginning in FY 12, the legislature eliminated the PILOTs and replaced them with manufacturing transition grants.

- If the State reimbursed towns for this tax loss at 100% like they did prior to FY12, it would more than make up for the assessment loss towns are seeing from the MV changes. If the reimbursement was a lower percentage amount than 100%, it would still provide critical relief.

-

Work with the Connecticut Association of Assessment Officers (CAAO) to amend language in PA 24-46 to include an application & application deadline, direction on who is responsible for creating an application, address the home ownership percentage, life use, a 100% disability rating from the Veteran’s Administration, and a cap on the total exemption amount.

- Consider increasing the motor vehicle mill rate cap from 32.46, which would give municipalities the ability to apply a higher mill rate to the lower motor vehicle values. This would also reduce the State’s burden to reimburse municipalities under the MV Cap Grant since RE and PP mill rates will not have to increase by such a large amount to offset the MV value losses.

-

As always, thanks for all you do on behalf of the residents of the State of Connecticut.

Respectfully,

Kevin Redmond

Director of Finance, Ridgefield, Ct

Connecticut Government Finance Association President

Cc: